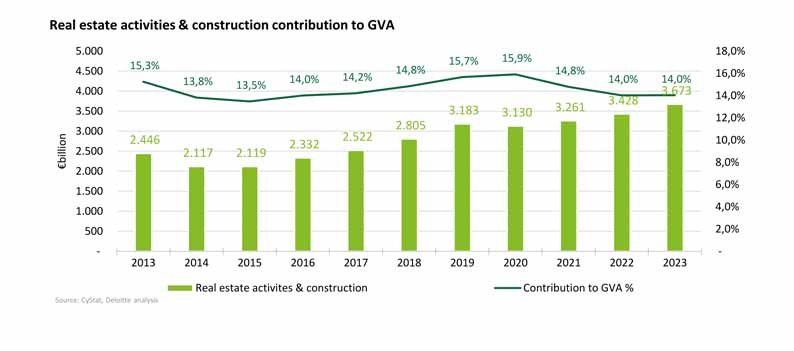

The Cyprus real estate market is steaming ahead and far from cooling down, as 2023 closed with 25,400 transactions worth €5.6 bln, according to a study by Deloitte.

The ‘Big Four’ audit and advisory firm released the Cyprus Real Estate Review, offering a comprehensive analysis of the market’s performance in 2023 amidst significant economic events regionally and globally.

According to the report, residential transactions were the driving force of the industry, representing 61% of the total market value (€3.4 bln from 13,200 transactions).

Vacant land transactions followed closely, contributing €1.9 bln across 11,200 transactions, maintaining stability in total sales, despite increased transaction volume compared to 2022.

Vacant land transactions followed closely, contributing €1.9 bln across 11,200 transactions, maintaining stability in total sales, despite increased transaction volume compared to 2022.

Commercial real estate transactions, while fewer, saw higher values, totalling €121 mln, comprising 2% of the sector’s total value.

Limassol continued to lead district-level performance, contributing 41% of total sales in value.

Other towns, except for Larnaca, experienced slightly lower sales compared to the previous year.

Larnaca enjoys remarkable increase

Larnaca stood out with a remarkable 28% increase in sales value, driven by both increased transaction volume and higher average transaction value, marking its third consecutive year of growth.

Survey results from Deloitte Cyprus indicated industry professionals expect minimal changes in the real estate landscape in 2024. Apartments remain the preferred investment choice, though luxury apartments in high-rise developments may see a decline.

George Martides, Financial Advisory and Real Estate Industry Leader at Deloitte Cyprus, emphasised the sector’s resilience despite economic pressures like inflation and interest rates.

He stressed the importance of addressing future challenges such as sustainable development, technological advancements, government reforms, bureaucracy, and affordable housing through collaboration between the public and private sectors.

“These results instill optimism, but also a sense of responsibility to effectively address any future challenges – such as sustainable and green developments, the rapid growth of technology and artificial intelligence (AI), government reforms, bureaucracy, affordable housing – and to intensify our efforts in attracting new types of investment from both foreign and local investors,” said Martides.