As the energy crisis deepens and the omens for 2023 are not good on the supply front, much soul-searching is now taking place among politicians, Eurocrats and energy analysts.

In the aftermath of Russia’s incursion in Ukraine last February, the energy scene in Europe has changed radically following the decision by the US and the EU to reduce Russian energy imports to a minimum.

Most profound has been the substitution of Russian gas supply with increased LNG imports from the US, Qatar and elsewhere and higher volumes, via pipeline, from Norway and Algeria.

The EU’s unilateral decision last March to press ahead by all means and against all costs to decouple from Russian energy – crude oil, oil products, natural gas and coal – over a short period has upended long-term supply contracts worth hundreds of billions and forced European businesses to look elsewhere for energy supplies.

The accelerated change of Europe’s energy direction has also come at a huge cost following a sharp rise in electricity and gas prices in almost all of the 27-nation bloc and the UK.

Gas prices have jumped on average eight times above early 2021 levels, and electricity prices, which are directly affected by gas, have similarly experienced manifold increases.

The governments of most European countries have resorted to heavy subsidies to prevent wholesale electricity and gas prices translating into extravagant retail energy prices, which could have led to social upheaval.

According to estimates by the Bruegel think tank, the total cost of the energy crisis in the EU is likely to have reached a total of €1 trln by the end of 2022, of which €700 bln corresponds to consumer subsidies of one form or other.

As the current energy crisis persists, it is becoming abundantly clear that this is the result of an actual supply shortage, especially in the case of European gas.

As Russia has gradually suspended deliveries in many countries, the resulting gap had to be filled by increased liquified natural gas (LNG) imports, the cost of which is much higher than the one applied to long-term gas supply contracts that many countries had with Russia’s Gazprom over the last 40 years or so.

In 2021, Russian gas exports to the ‘EU 27’ amounted to 153 bcm, of which 137 bcm were delivered via pipeline and the rest as LNG.

Russian gas imports correspond to almost 37% of EU gas supply and 46% of total gas imports.

According to preliminary estimates, there has been a dramatic fall in Russian gas export volumes in 2022 to the EU, totalling 70 bcm.

To meet demand, which has dropped only slightly, EU member states increased their pipeline imports from Norway and resorted to massive LNG imports, mainly from US, Qatar and Algeria.

In a sense, they exchanged one form of dependence with another and were more expensive.

As Russia is expected to further curtail gas exports to Europe in 2023, the outlook is for more LNG imports.

The European Commission is actively searching for alternatives including increased gas deliveries via pipeline from Azerbaijan and Algeria.

Until recently, Europe’s huge dependence on Russian gas imports indicates the continent’s worsening energy predicament.

According to the latest Eurostat data, in 2020, the EU was 60% dependent on energy imports of all kinds, with the highest that of crude oil, followed by gas and coal.

In the case of gas, the EU’s dependency increasingly worsened over the past 20 years as indigenous production in the North Sea and the Netherlands – mainly from the Groningen field – got progressively less.

Last year, total European gas production reached 50.6 bcm, corresponding to just 12.3% of total consumption.

Hence, if Europe wants to rein on unrealistically high gas prices and do away with massive fiscal subsidies which only help distort market competition and encourage consumer complacency, it has to take bold steps to increase production from local sources within member states.

Although encouragement of European gas production runs contrary to the much-touted green agenda of the European Commission, which aims at curbing significantly oil and gas use by 2030 as it heads towards NetZero50, the ferocity and tenacity of the current energy crisis are such that a major repositioning of energy policy seems inevitable.

Already, we see signs of this change in energy policy as the emphasis has been placed lately on the construction of new LNG and gas storage facilities, especially in Germany, the Baltic countries and SE Europe.

In contrast, more companies are entering into long-term LNG supply agreements with the US, Qatar and other major producers.

Such contracts normally run for 15 to 25 years, well beyond the time limit set by ambitious EU goals for the continent’s decarbonisation.

Cyprus

In this context, Cyprus and other countries in the East Mediterranean, notably Israel and Egypt, have an important role in ensuring European gas supply from a region bordering the main European land mass.

Let’s consider all the EU’s indigenous or near-indigenous gas sources.

We shall see that between them, the North Sea, the Adriatic, the Black Sea, the Ionian Sea, the Cretan Sea and the East Mediterranean (including Cyprus and Israel) have proven or contingent hydrocarbon reserves estimated to exceed 12 trillion cubic metres which can cover European gas consumption for 30 or more years.

They could stretch for many more years as gas consumption is likely to level out or even decrease over the coming years as energy efficiency measures take hold, more fields are discovered, and gas imports from LNG and pipelines from friendly countries are likely to continue, albeit at a lower rate.

Over the last ten years, important gas discoveries in offshore Cyprus are helping bolster the island’s role as a prospective major gas supplier to the EU, along with Israel and Greece.

The latest gas finds at the Zeus location in block 6, operated by ENI, just before Christmas, concerns an estimated quantity of 2.0 to 3.0 trillion cubic metres (tcf).

Although small in volume (at 72 billion cubic metres) compared to other gas discoveries in the East Mediterranean, the particular find is a positive addition to the rest of the gas discoveries in offshore Cyprus.

The Zeus discovery brings the number of deposits off Cyprus to five and includes findings in Blocks 6 (Cronos and Zeus), Block 10 (Glaucus), Block 7 (Calypso) and Block 12 (Aphrodite).

Between them, these fields are estimated to hold proven reserves amounting to 15.2 to 18.2 tcf or 570 to 655 bcm.

Suppose we were to examine Cyprus’ growing hydrocarbon natural gas potential in a broader regional context, especially in relationship to Israel, which has proved reserves nearing 1 trillion cubic metres.

In that case, a picture emerges whereby the Israel-Cyprus axis could develop into an important alternative gas supplier to Europe.

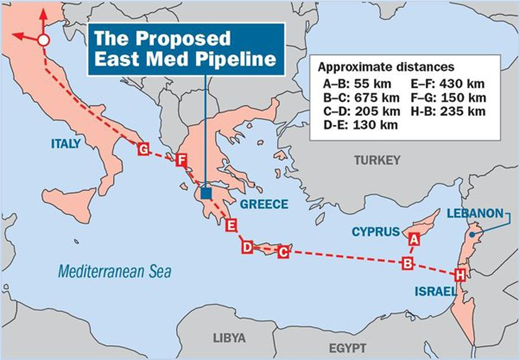

Gas exports from the region towards European destinations can be secured either through liquified natural gas (LNG) shipments or through the planned EastMed Pipeline (see map).

Although this project has over the past years attracted considerable criticism from various quarters – notably from Turkey and the US – on account of its routing and high cost, the current energy security situation in the EU is such that Brussels is keen to promote the project, which after all is a fully backed European Project of Common Interest, as a matter of urgency.

The huge price differential between current gas prices in the East Med and continental Europe makes the importation of gas from this region a bankable proposition since long-term gas purchase agreements can now be established between sellers (Israel, Cyprus) and buyers (EU countries).

Costis Stambolis is a Financial Mirror correspondent based in Athens