By Costis Stambolis

As Cyprus has embarked on the road to introducing natural gas to its energy system, following the signing of agreements by DEFA – Cyprus’s gas company – with contractors and suppliers last July, attention is now shifting on the role that gas is expected to play in the island’s economic development. According to the timetable presented by Simeon Kassianidis, DEFA’s chairman, at the 8th Cyprus Energy Forum on December 15, construction and mooring of the €300 million FSRU type LNG terminal to be located in Vasilikos, will be completed by autumn 2022 when first gas deliveries are scheduled.

Gas will then be channeled on a priority basis to the Vasilikos power station complex run by the Electricity Authority of Cyprus (EAC).

The thermal power stations run by EAC, which at present use highly polluting fuel oil, will switch to gas, thereby slashing their GHG emissions by at least 50%. Subsequently, the rest of the power stations operating on the island will convert to gas as this is mandatory, according to EU directives, in order to lessen their environmental impact.

However, natural gas will not be restricted to power generation, but will gradually be introduced to satisfy a wide variety of energy needs such as space heating and cooling, industrial processes, commercial use, cooking and co-generation.

According to DEFA’s plans, an extended network of main gas pipelines and city grids will develop over the next decade which will enable the efficient and safe distribution of gas in most parts of the island. In addition to the environmental benefits that gas will bring, it is most likely that it will lead to a more competitive pricing environment as natural gas costs are usually 70% or less compared to fuel, heating oil and diesel which are now widely used in Cyprus.

The arrival of natural gas and its entry into the energy mix of the island in two to three years’ time will no doubt constitute a monumental step forward in terms of energy use, a kind of paradigm shift, and must therefore be seen in context of what else is happening right now in Cyprus’s energy scene.

An equally important change is the gradual entry into the electricity mix of power generated by Renewable Energy Sources (RES) such as solar photovoltaic and wind power.

With some 300 MW of installed capacity RES, representing 17% of total installed capacity, they are already providing some 10% of the island’s electricity needs, a figure which is likely to grow substantially as installation and production costs have fallen dramatically over the past years.

Cyprus’s growing role in East Med

With Cyprus becoming the latest country in the region to obtain its gas supplies through LNG, its role is now being assessed in the broader context of East Med economic and political developments.

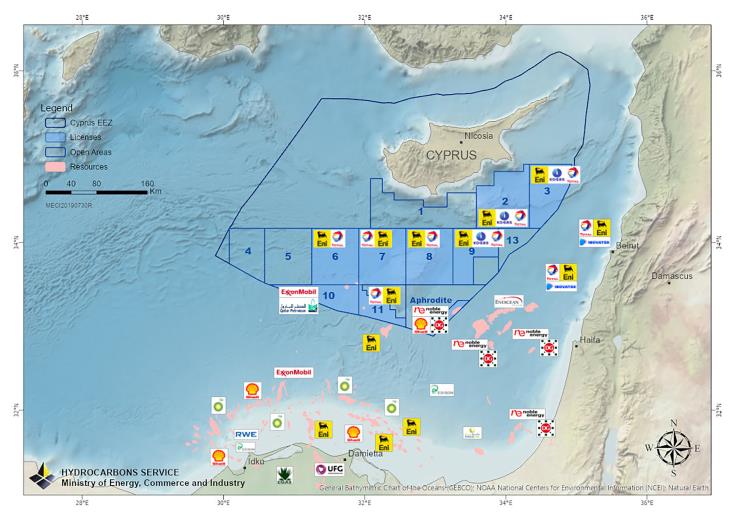

Having failed to develop on time the Aphrodite gas field, which was discovered in Block 12 (see map) back in 2011, and tap its considerable gas deposits – estimated at approx. 125 bcm – for domestic use and exports, the Republic of Cyprus had no other option but to press ahead with the introduction of LNG in order to help decarbonise the island’s energy system.

Having failed to develop on time the Aphrodite gas field, which was discovered in Block 12 (see map) back in 2011, and tap its considerable gas deposits – estimated at approx. 125 bcm – for domestic use and exports, the Republic of Cyprus had no other option but to press ahead with the introduction of LNG in order to help decarbonise the island’s energy system.

At the same time, the Cyprus Hydrocarbons Company has concluded an agreement with overseas buyers to export gas from Aphrodite to the Idku liquefaction terminal in Egypt in order to monetise the field’s gas production from 2023 onwards.

Following three international licensing rounds from 2007 until 2018 which involved 8 out of the 12 sea blocks available for exploration, some of the world’s leading energy companies, including Exxon Mobil, ENI, Total, etc., have been awarded exploration and production licenses in offshore Cyprus waters with 3 major gas discoveries reported so far.

With 4.1 TCF of recoverable reserves and 8.0 -12.0 TCF estimated or in place, the outlook for developing the island’s substantial natural gas reserves is more than promising.

Although oil and gas prices have fallen sharply over the last few months, as a result of demand contraction due to the pandemic, there are now clear signs of recovery as demand resumes. The shadows thrown over the long term by the EU’s over-ambitious green agenda which excludes gas, the use of gas is not really touching Cyprus as this is an international commodity and future production is most likely to be absorbed by increased use in the rest of the world.

LNG attracting investment interest

When it comes to LNG, its growing importance in the East Med as the fuel of choice in meeting rising regional demand is attracting high investment and commercial interest.

In the past decade SE Europe and the eastern Mediterranean have attracted the attention of many global players who are seeking investment opportunities in both upstream and midstream projects, including LNG.

Despite the growing role of RES and the consequent shifts in the energy mix, LNG is clearly emerging as a “transition fuel” in SEE and east Mediterranean countries.

The expansion and upgrade of existing LNG receiving terminals, along with the development of brand new LNG projects, such as the one at Vasilikos, and other critical supply and interconnections, are gradually changing the energy picture in the region, enhancing gas supply security, and provide substantial opportunities for diversified LNG supplies.

With Turkey and Greece being the main LNG importers in SE Europe, Cyprus is a relatively latecomer onto the scene.

This is not necessarily a disadvantage as prices have fallen following a global LNG supply glut.

Turkey having massively invested in LNG receiving terminals – both onshore and FSRUs – benefits now from an LNG glut and low prices. Similarly, Greece, thanks to the Revithousa LNG terminal, has painlessly overcome the consecutive Russian-Ukrainian crises and gas supply interruptions of the past. After the terminal’s upgrade, it not only benefits from LNG oversupply and low prices, but is also closer to its strategic ambition to becoming and LNG gateway and regional price setter for SE Europe and the East Med.

With Cyprus now moving into the LNG era this can only enhance its position as an energy trading post while enhancing its security of energy supply.

Costis Stambolis is a Financial Mirror correspondent, based in Athens