By Naeem Aslam

European and US markets are trading with caution as investors and traders wait for one of the most important economic events. Fed Chairman Jerome Powell is scheduled to deliver his testimony at Jackson Hole on the second day of the summit.

His approach could be similar to Thursday’s, maintaining a cautious stance. The Fed Chair’s important job now is to not give any false hopes to the market, while managing expectations with a fine line.

It is pretty much a done deal that the Fed will cut the rate in September, as was evident in his comments and also in the Fed minutes released earlier this week.

The actual monetary policy event that will take place next month would very much be a non-mover for the US equity markets and investors around the world, as the US is the largest equity market in the world, and hence there is a massive spillover effect in terms of sentiment.

In terms of the US economy’s health, we got a further glimpse when the economic data printed a bit of a mixed picture.

For instance, the Flash Manufacturing PMI number is still very much in contraction territory, as the print confirmed the reading of 48, while the Flash Services PMI number produced a better-than-expected value of 54. The actual print was 55.2, and this boosted confidence among traders.

The weekly jobless claims were the more important economic number for this week, as the US job revision data confirmed a loss of momentum among traders and investors.

The US weekly jobless claims actually matched expectations, and this was a positive sign for those who were worried about a slowdown in the job market.

Remember, in the Fed Minutes and Jerome’s speech, the theme was the same: downside risk to the job market and upside risk to inflation, so the tailwind is not really in favour of the Fed, which means that they would have to take every action with even more caution.

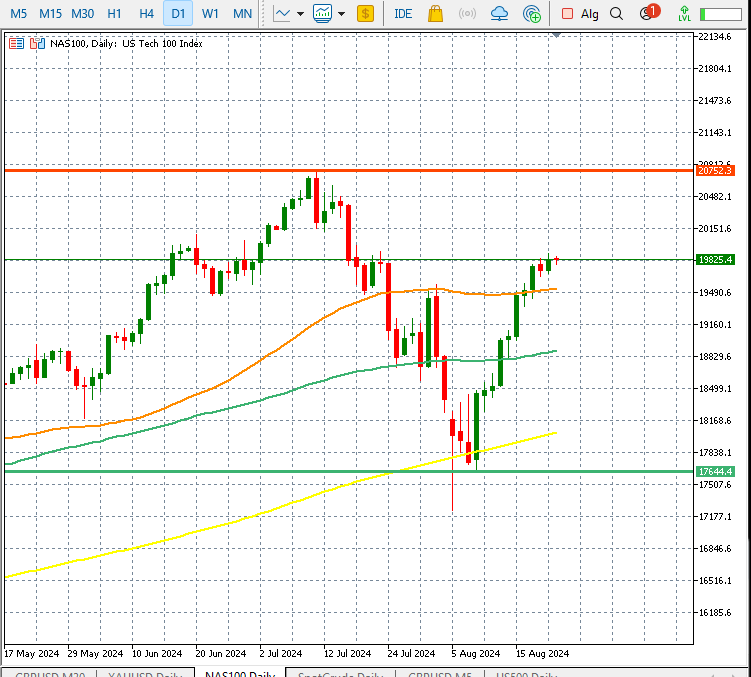

Technical Matters

The Nasdaq’s, US 100 chart below shows that the bulls are in control of the price action as the price has moved above the 50, 100 and 200 day SMA on the daily time frame.

The important support and resistance levels are shown on the chart.

Sterling On the Move

After the UK’s manufacturing PMI and services numbers exceeded expectations, surpassing those of any other European economy, attention is once again focused on the Bank of England and its potential next move.

The bank has already lowered the interest rate in its last meeting, and now expectations are what the bank will do at its next meeting.

The Bank of England’s governor will be speaking later Friday, and the focus will primarily be on the bank’s monetary policy and possibilities of another rate cut in September. If there are any hints of a rate cut, we could see some wind coming out of the Sterling rally, which has been moving to the upside on the back of economic data, and vice versa.

Gold Set To Record Losses

The price of precious metals is on track to record some losses for the week, but it has moved lower.

Currently, there are expectations that the gold rally will continue as the Fed cuts rates in September. However, traders must understand that the rate cut of 25 basis points has already been factored into the price. Therefore, the actual event could negatively impact the gold price, as traders would not perceive it as a bullish event.

On Thursday, when Jerome Powell delivered his first speech at Jackson Hole, the market did not respond positively, as there were no indications that the Fed would adopt an aggressive strategy to lower interest rates.

A gradual interest rate cut may help, but the timing of the next rate cut is an important one, and this is what traders and investors will be looking for when Jerome Powell comes into the spotlight again.

Naeem Aslam is Chief Investment Officer at Zaye Capital Markets.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Zaye Capital Markets.