By Naeem Aslam

Investors and traders continue to support riskier assets, while the focus among them is very much on earnings and economic data.

The fact that the Dow Jones industrial average has posted its fourth consecutive winning session — the longest winning streak in weeks — has lifted spirits among traders who think that the days may be numbered for rates to remain higher for longer.

European markets are trading higher, and most of the European indices are well on track to post their weekly gains.

Investors are taking comfort in the fact that the retail sales data in Europe, which very much shows the naked form of consumer confidence, produced a much better reading on Tuesday as compared to expectations (actual was 0.8% while forecast was for 0.6%).

However, there are plenty of soft spots in the economic data, and traders should practice caution when being overly optimistic about things. For instance, German Factory Orders m/m, at -0.4% is against the forecast of 0.4%. Of course, the number was much better when compared to the previous reading, which came in at -0.8%.

As for the UK, traders are eager to hear some sort of good news from the Bank of England, which will come to light on Thursday as the bank will announce its monetary policy.

We anticipate no interest rate change. However, the hope is that we will hear more positive news in terms of interest rates from the BoE.

The UK’s growth story is weak, posing real threats of stagflation as consumers continue to struggle to meet their everyday expenses. We expect them to shift their current narrative towards a more hawkish monetary policy. For example, traders anticipate a change in the official MPC bank rate.

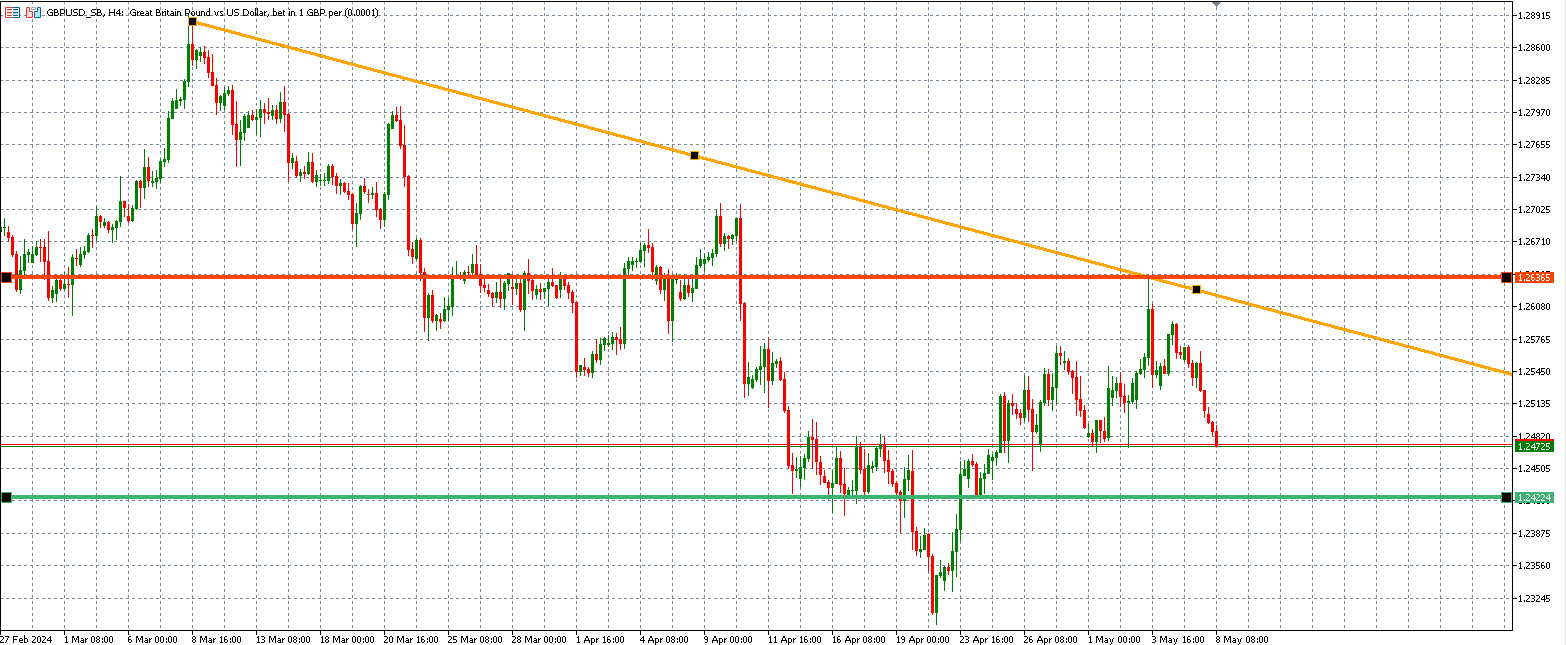

The GBPUSD chart below indicating that a change in the BoE’s monetary policy stance is coming and rate cut is on the table sooner than later. The important support zone is shown by the green line and the resistance is shown by the red line.

US focus on earnings, Disney in the spotlight

Over in the US, continue to focus on earnings. Disney, which produced a somewhat less stellar number Tuesday night, remains in the spotlight.

If we look at Disney’s numbers, we do not think that the numbers missed expectations by a mile; in fact, given higher inflation, constant pressure on costs, and higher wages, the company has done well.

But traders and investors are concerned about their streaming business, which is in a very competitive landscape, and content and cost are the two most important ingredients to which everyone is paying close attention.

With so much competition in this space, the company that maintains the right mix of these two factors will emerge as the winner.

In the commodity space, gold continues to dip lower as investors assess and digest the recent commentary from FOMC members. If we look at their messages, it is still unclear if the Fed is going to do anything about interest rates, despite the fact that the labour market data produced a poor number last week.

The lack of supportive comments for a lower interest rate made traders feel more confident about the dollar index, which has gained strength. The higher moves in the dollar index are causing the gold price to drop.

Gold awaits key data

Thursday’s weekly jobless claims will be the economic number that is likely to bring moves in the gold price, as they are going to shape the next payroll data and the Fed’s monetary policy.

Further weakness in these numbers could push the dollar index lower as traders become worried about the health of the US economy, which should make the Fed move the needle on its monetary policy. All of this should boost gold prices.

On the flip side, any strength in these numbers could make traders support the dollar index, thus taking more shine away from the yellow metal.

Naeem Aslam is Chief Investment Officer at Zaye Capital Markets.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Zaye Capital Markets.