By Moody’s Analytics

The June U.S. consumer price index has financial markets increasing their bets on a 100-basis point rate hike at the upcoming meeting of the Federal Open Market Committee.

The CPI increased 1.3% in June, more than our above consensus forecast for a 1.2% gain. June’s increase leaves the CPI up 9.1% on a year-ago basis. Inflation is likely moderating this month because of the drop in energy prices, so inflation won’t remain above 9% for long.

However, the Fed isn’t getting the clear and convincing signs that inflation is decelerating. It needs to see those signs before it slows rate hikes.

After the CPI release on Wednesday, Fed swaps put the odds of a 100-basis point rate hike at 50%. The debate is now whether the Fed will raise by 75 or 100 basis points.

There’s a difference between what the Fed can do and what it should do. Hiking by 100 basis points would reduce the odds of the Fed engineering a soft landing, unless it pauses after returning the fed funds rate to 2.5%, its estimate of the neutral fed funds rate.

The issue facing the Fed is that, even though there is a lengthy list of forces driving inflation higher, the massive shocks to the supply side of the economy, including the Russian invasion of Ukraine and the COVID-19 pandemic, are far and away the most important. The removal of monetary policy accommodation will not solve the supply side issues that are behind our inflation problems.

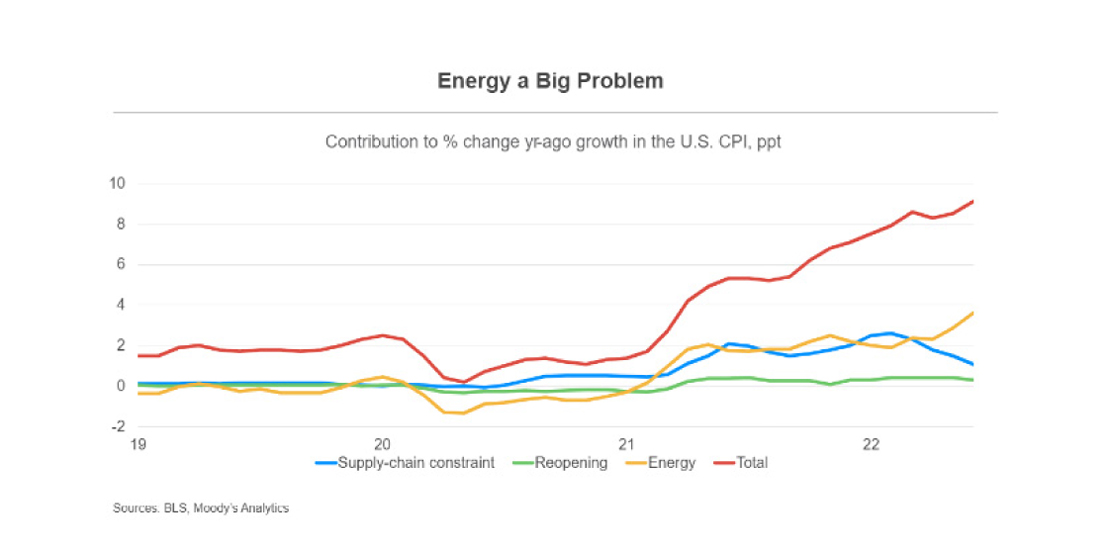

Energy continues to be an enormous source of inflation.

Energy services prices were up 3.5% in June with electricity and utility gas services prices both rising. Ahead of the June CPI, anecdotes showed that providers were boosting utility prices. The CPI for energy added 3.6 percentage points to year-over-year growth in June.

Better news

There was some better news on supply-chain-linked inflation.

Supply-chain-constrained components of the CPI added 1.1 percentage points to year-over-year growth in the CPI in June, less than the 1.5-percentage point contribution in April and the smallest since March 2021.

In fact, supply chain issues have been adding less and less to growth in the CPI recently. Reopening-sensitive components of the CPI added 0.3 percentage point to growth in the CPI in June, less than the 0.4-percentage point contribution in each of the prior four months.

Excluding energy, supply chains and reopening, year-over-year growth in the CPI in May would have been 4.1% compared with 3.7% in May.

Costly and sticky

The typical American household now needs to spend $493 more per month to buy the same goods and services as it did last year.

Some of the acceleration in inflation is attributed to rents, which are sticky. The CPI for owners’ equivalent rents rose 0.6% for the second consecutive month. The CPI for rent of primary residence increased 0.8%, stronger than the 0.6% gain in May.

Owners’ equivalent rents were up 0.7%. Rents are normally fairly sticky but will continue to accelerate, and growth should peak this summer. Still, the CPI for rent added 1.9 percentage points to year-over-year growth in the headline CPI, the most since the early 1990s.

We knew that rental inflation was going to be an issue this year but assumed that was going to be more than offset by goods disinflation.

However, the disinflation in goods prices has been more gradual than anticipated. This could be an issue for the Fed, as rents will continue to rise, making it difficult for the central bank to have clear evidence that inflation is decelerating and removing the potential for a pause in the tightening cycle.