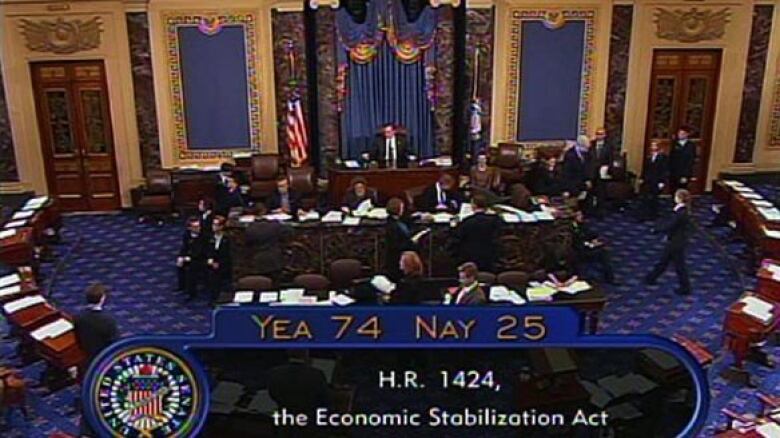

The U.S. Senate approved a $700 billion bailout of the financial industry, putting pressure on the House to approve a plan that political and financial leaders called crucial to averting economic castastrophe.

The revised legislation is aimed at reinvigorating worldwide credit markets and interbank lending that had frozen up while overleveraged financial institutions staggered under the weight of failed mortgages.

But market participants warned that the rescue package is not a cure-all, with a worsening economic outlook spurring calls for central banks to cut interest rates.

Stocks in Asia were lower on Thursday on recession fears, and European stocks were also forecast to open weaker. Treasuries rose and the dollar gave up early gains.

“Even if the bill is passed, worries remain over the global economic outlook so financial markets are unlikely to stabilize,” said Masamichi Adachi, senior economist at JPMorgan in Tokyo.

“It’s a completely different world now. All the things U.S. authorities are doing now are simply aimed at preventing a global meltdown.”

Amid warnings that failure to act could plunge the country into a depression, the Senate voted 74 to 25 in favor, sending the measure to the House of Representatives, probably for a vote on Friday.

U.S. President George W. Bush praised Senate passage of the package and urged the House to quickly do the same.

“With the improvements the Senate has made, I believe members of both parties in the House can support this legislation,” Bush said in a written statement. “The bill the Senate passed is essential to the financial security of every American,” he said.

HOUSE PASSAGE SEEN MORE LIKELY

Leaders in the U.S. House of Representatives, where Monday’s “no” vote rocked global markets, expressed cautious optimism that the legislation would be approved.

Senate leaders hope that sweetening the plan with a tax cut and extended federal protection for bank deposits can turn “no” voters into supporters. On Monday, the House rejected the previous version of the plan by a 228-205 vote.

“It’s still uncertain. I think it is likelier to pass than before,” House Financial Services Committee Chairman Barney Frank said in an interview on CNN.

“The main change is reality. I think that it’s not possible now to scoff at the predictions of doom if we don’t do anything,” the Massachusetts Democrat added.

Many Americans resent the idea that Wall Street is being “bailed out” at taxpayer expense, and have made their views clear in emails and calls to Washington, putting pressure in particular on vulnerable members of the House of Representatives.

All 435 House seats will be contested in the election on Nov. 4, as opposed to 35 seats up for grabs in the Senate.

Treasury Secretary Henry Paulson, whose original three-page proposal grew to hundreds of pages when Congress got involved, praised the Senate vote and urged the House to act swiftly to ratify it.

Should the House uphold the bill, it would go to the White House for signature into law by President Bush.

“This sends a positive signal that we stand ready to protect the U.S. economy by making sure that Americans have access to the credit that is needed to create jobs and keep businesses going,” Paulson said.

The financial crisis has become the biggest issue in the upcoming U.S. elections, and both presidential candidates, Republican Sen. John McCain and Democratic Sen. Barack Obama, voted for the package.

Stocks in Tokyo dropped 1.9 percent on Thursday, while MSCI’s share index for the rest of Asia lost 1.2 percent. Oil gained $1 a barrel.

The credit crisis reverberated among European banks while recessionary signals mounted in the United States.

U.S. factory activity shrank in September to its lowest since the 2001 recession and major automakers reported plunging U.S. sales for September, led by a 34 percent slide at Ford Motor Co

“If the massive expansion of the Fed’s balance sheet and other CB (central bank) liquidity injections cannot do the trick then coordinated global rate cuts becomes likely and necessary,” Michael Hartnett, chief emerging markets equity strategist at Merrill Lynch, wrote in a note.

In Europe, France and Germany clashed over the idea of a U.S.-style financial rescue fund for Europe amid further signs of contagion from the global credit crisis.